A opportunity to invest in a small-cap Canadian trucking company with immense growth potential amidst a deflationary phase of the transportation cycle and depressed valuations

Investment Thesis & Conclusion

An opportunity to purchase a lesser-known Canadian trucking company with a 2x margin of safety on its earnings yield, and participate in a long-term Canadian trucking growth story for potentially 50c on the dollar owing to short term macro and industry headwinds. I strongly recommend that the equity of the company may be bought as a portfolio holding at a purchase price at or below $2.50 in order to maximize the realization of a 15% CAGR on the equity over a 5-year period assuming a 5-year target price of $5.02.

Hard Catalyst

Continued synergistic acquisitions by TTNM to boost topline and earnings growth to help drive margin expansion on completion of integration whilst maintaining a strong balance sheet to weather short term headwinds.

Soft Catalysts

- Market Cap growth allowing more mandates/funds to invest in the capital structure / equity of the company

- Potential addition to the TSX Index

- Attrition of less healthy trucking companies (YELL US etc.) helping prop up pricing

- Multiples expansion of TTNM in tandem with growth of market cap to attain similar multiples to the bigger businesses such as KNX US, TFII CN (currently ~20% discount)

- Recovery of general business conditions leading an inflationary cycle of the trucking industry

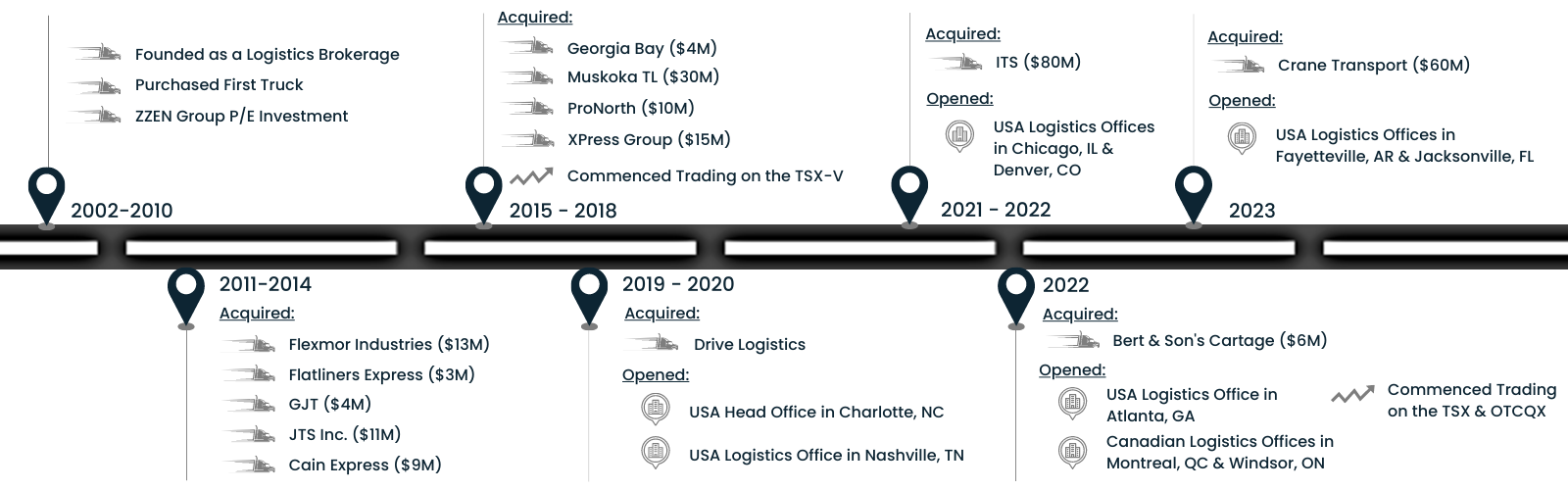

Company Background

The company provides asset-based transportation (LTL, FTL) and logistics services across North America, with an almost 50-50 split in revenue among both – the operational segments as well as by region. The company was founded by Ted & Marilyn Daniel in the year 2002 before going public in 2015. It graduated to the big board from the TSX-V in 2022.

TTNM currently trades at a PE of 7x, PB of 1.24x and EV / EBITDA of 3.32x. Led by a formidable CEO who spent 10 years in the trucking industry before founding TTNM, the company has recently completed an acquisition in the US (Crane Services) via cash on hand and a take-back loan. It presently operates terminals, warehouses, and brokerage services across the USA and Canada – with plans to expand further into the US to help topline and free cash flow growth. TTNM presently has a debt to equity of 1.42 and Net Debt / Equity of 1.18.

The company has been growing its topline at a 20%+ CAGR over the last five years and given the current economic headwinds and depressed valuations, is well positioned to make use of its balance sheet to help further growth and ride the crest of the next economic cycle. Given the product mix of the company – which is tilted towards CPG and F&B, it has enough buffer to stabilize revenue in choppy and uncertain economic conditions.

Product and Growth Plans

Given the commoditized nature of the industry and the business, it is imperative to seek managed growth by acquisitions as well as focus on the technological aspects of the brokerage division to enhance margins. Given the same, management has proven itself to be astute capital allocators and have engaged in more than 10 acquisitions over the last 5 years and intend to complete three more acquisitions in CY2024 as briefed by the CFO during the most recent earnings call. It is the intention of the company to become a $1B+ topline company in the near future. Owing to the fragmented nature of industry and distribution routes in Canada, as well as monopolization by region, the near-term focus of TTNM will be to branch out and grow south of the border – where the $1 trillion industry is expected to grow at a 4% CAGR. This has set up the company fairly well.

Current Economic Outlook and Macro Factors

The highly fragmented industry is presently in the deflationary trough as may be seen by the spot and contract rates (see below), combined with the contraction and equalization of the Industrial Production and the Sales to Inventory ratio. Although unclear, irrespective of whether the economy enters a soft landing or a recession in the near term, it may be assumed that unlike the post-COVID boom & inflationary cycle – where freight demand was driven by an increase in purchases and demand for goods as well as congested supply chains and falling inventory levels, it may be assumed that the commencement of the next inflationary cycle will be driven by attrition of the weaker incumbents and freight capacity (a recent example being YELL US: Yellow Corporation) instead of exceptionally high demand.

Furthermore, stabilization of the current trucking supply demand economics may be compared to the 2019 or even 2013 levels when extrapolated by the Class 8 (heaviest truck) used truck data.

The prospects of a soft economy or a full-blown recession are already being seen by some of the price action of the larger-cap trucking companies – which typically serve as a leading indicator of the economy (adjusting for the bankruptcy of Yellow Corporation giving a short-term fillip). This brings us to the present opportunity presented to us by the vicissitudes of the trucking industry as well as the compression of the multiples and valuations of publicly listed companies in this business.

Valuation & Current Opportunity

Given the current downturn in the markets and compression of multiples a very conservative approach has been utilized to estimate a safe purchase price for TTNM CN. Further, given that the company is still in its infancy and growth stages – which will entail subsequent and a fair amount of deals over the next five years (whose timing is difficult to anticipate and therefore accurately model out), it would be a mis-step in the authors opinion to try and estimate the equity value via a discounted cash flow method (DCF) owing to the uncertainty of the CapEx spending as well as the sensitivity to the terminal value and by extension the EBITDA / exit multiples. Similarly, given that the company is relatively small compared to the larger incumbents – which would entail a multiples discount owing to coverage and liquidity issues among other things, the author presumes that it may not be intelligent investing to value TTNM CN using peer multiples at this present time. Owing to the same, an Income Based Valuation approach has been utilized which allows us the use of the (normalized) historical track record of the company to extrapolate a conservative growth rate over the next five years. Although the company has grown its topline rapidly over the last 5 years (>25%) and is in its growth stages a conservative 15% growth rate has been assumed with a 3.3% earnings margin – another conservative estimate from historical precedents of 5%+.

The WACC which was backed out for the company from the debt and equity cost, using a 1.5 beta value, will be used for illustrative purposes as compared to being used for decision making – considering that as intelligent investors we are looking to arrive at a safe cost basis to build up our position.

Thus, for a ‘28E EPS of $0.63, the following equity value for TTNMs common stock is arrived at, which averages out to $7.81. The average may be used as a rough indication of the normalized long-term P/E based valuation and target price average for the company.

Discounting back to today, using the 15% hurdle rate we arrive at a normalized equity value of $3.88 per share (see image below) for TTNM. It is to be noted that the 15% hurdle rate column indicates the required cost basis to arrive at a 15% CAGR 5Y return for holding the company equity (with the indicated line item target prices displayed in the above image). Given that very conservative values for topline growth and net income margins have been used, especially given that margins will likely expand once the company climbs out of its growth stages and all arms of the business synergize completely – it would be moot to discount the arrived at equity values any further and introduce an “artificial safety margin” so as to avoid double counting of risk factors.

The average of the highlighted values gives us $2.45 (see image below) which has been rounded up to $2.50 (which implies an 18% topline CAGR or a corresponding growth in multiples) as the upper limit to accumulate and build out the position in the company as of today. Changes in growth and margins estimates, would require re-adjustment of the thesis and entry points. Furthermore, cost basis assumptions would also need to be adjusted to account for various factors such as investor risk appetite, time horizon for investing and personal requirements.

Thesis Strengths

- Strong management, with equity sharing plan for employees provides an opportunity for stakeholders to buy-in to the company and shows an ownership tilt. Founders own close to 8% of the company

- Active NCIB. Company has repurchased $1.5MM worth shares recently, however, it many be noted that a portion of the same has been offset by option grants to Directors

- Young company which is still growing and the trucking industry is fragmented creating opportunities to grow

- The company generates between 6 – 8% CFO as a percent of topline. CapEx over the long term would need to be balanced (i.e. M&A and average age of fleet) to avoid liquidity issues. This should be arrived at once the pace of M&A slows down and margins expand leading to more CFO and lower CapEx and therefore greater free cash flows.

Thesis Weaknesses / Risks

- The company’s going concern status and liquidity depends largely on the management’s competence and avoidance of tail risk events given the relatively higher amounts of leverage involved during the growth stages of a business in a fragmented industry

- CapEx management by the leadership is paramount, failing which the company may become burdened with excess leverage

- Unforeseen and foreseen circumstances combined with a high interest rate regime may lead to a breach of covenants and a technical default

- The assumption that the North American economies travel through a recession and re-commence an inflationary period in the trucking business may not play out in the expected timeframe (i.e. within 5 years from today)

- Multiples expansion of TTNM CN may not play out as expected especially in a weaker than expected economy and bearish sentiment over the longer run

References / Sources Used

- Fleet Equipment Magazine

- ATA

- Yahoo Finance

- SEDAR+ Financials and Filings of TTNM CN

- Earnings Transcripts

- Coyote Logistics Research

Disclosure: The author / I personally own shares of TTNM CN as a part of my PA. It also may be understood that the article does not construe investment advise or guidance and that all readers and participants need to undertake their own due diligence prior to making investments.

I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. No recommendation or advice is being given as to whether any investment is suitable for a particular investor.

Pingback: Portfolio Update: Actively Passive Investing | Sanket Karve