We close the month with the portfolio narrowly beating the index by 9bps since inception. With the FIFA World Cup looming, I reckon there are potential runners in the bag which will help the portfolio. Also, my thoughts on IHRT US fixed income offerings as well as investing actively to build a passive portfolio

Marketable Securities

The top five portfolio holdings are Fairfax (FRFHF), Berkshire Hathaway (BRK/B), Figs Inc. (FIGS), Vestis (VSTS), and Visa (V). The portfolio continues to hold Sabre Inc. (SABR), which has seen its weighting reduce owing to poor performance in the market. The company’s equity was purchased at close to $3.20 apiece, however it occupies a lower weight after being beaten down to a dollar share price (latest close at $1.18). The portfolio will continue to hold on to the shares of Sabre Inc. High-Yield bonds of IHRT have performed as expected so far with maturity being May 2026. I expect the bonds to yield close to 13.52% in a few months’ time. The portfolio also maintains a very miniscule exposure to the “Fannie Mae Pref Shares” which has also been a positive contributor to the portfolio.

After hours reading research, following funds, and working for a bit on Bay Street, it is my understanding that few funds manage to regularly outperform the index in a sustainable manner. It has been my mission over the last two years, to gradually build a portfolio which delivers superior performance to the index, whilst requiring as minimal effort as possible. The fact that there are no performance drags is a huge benefit. I firmly believe that with Fairfax & Berkshire being the cornerstones of the portfolio, SABR Inc. (SABR US) and Vestis (VSTS US) could prove to be long term compounders from today’s position. Titanium group will unfortunately be sold at a loss, owing to the recent MBO. One can’t blame management for being proactive, opportunistic and smart investors – what with taking the company private on a song. Here’s my write-up on Titanium Group posted a while ago.

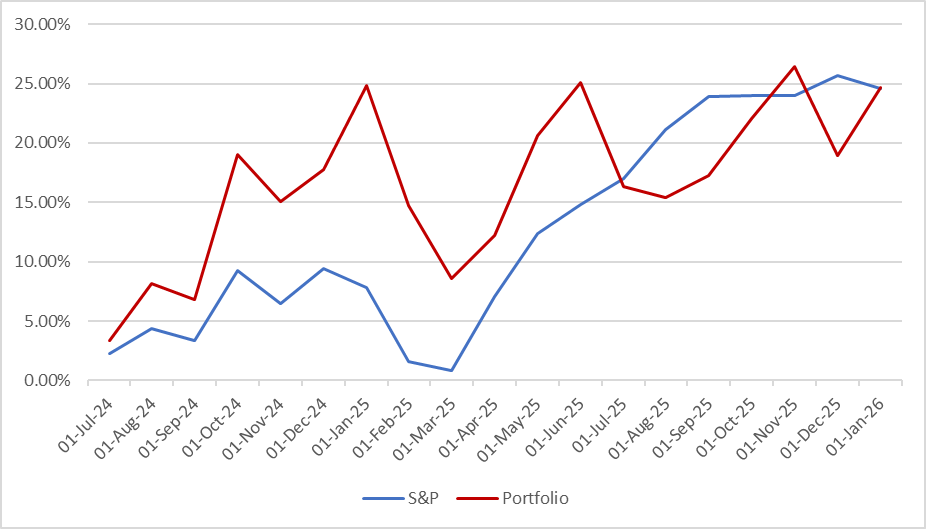

Actively Passive – Performance

As I have previously discussed, the plan is to set up the portfolio with six or seven core positions, with satellite holdings which will be tactical plays and making up the remainder 20% or so of the portfolio. The satellite holdings will involve fixed income, equity and option strategies which are nimble and tactical in nature, such as risk arbitrage, options writing, high-yield investments among others.

As can be seen, twenty months from commencing my plan, the portfolio narrowly manages to keep abreast of the index with a 9bps differential of performance (in the portfolio’s favor). Although most professional investors, and enthusiasts with investing as their night jobs try to aim for sky high returns, whilst maintain a high sharpe ratio (low volatility and steady returns), I am comfortable with the returns being “lumpy” – as can be seen from the chart.

As Anthropic, OpenAI, Nvidia and other AI firms take centre stage, and investors try to figure out whether markets are in bubble territory or in “just a phase mode”, my outlook remains sanguine. I believe the upcoming World Cup (Soccer) in North America will provide a boost to many businesses, Sabre being one of them. With the right management, debt handling and smooth running of business operations, I do believe that Sabre can turn out to be a multi-bagger given the company’s various characteristics. Figs turning out to be a four bagger in so short a time has been a pleasant surprise in the portfolio.

Given that I have mentioned Options Writing as one of the strategies which will be used in a tactical manner, let me devote some time to provide briefly, some more clarity on the topic. Readers can also refer back to a previous post where I discussed options writing and arbitrage as a comparative benchmark with the Corporate & Treasury yield curve.

Option Insurance for the Conscious Investor

To say that every investment is effectively competing with what one can achieve via fixed income, would be in my opinion, a very accurate statement. Whilst I have stated previously about my thoughts on Options writing, akin to writing or selling insurance on a stock with an implicit guarantee that the stock price won’t fall below or trade above a certain price point, let me elaborate a little further.

Based on a quick study that I have undertaken (with an admittedly small sample size), it appears to me that the duration of an option, i.e. the time between opening and closing an options position is negatively correlated to the annualized returns one can derive. This may also be explained by the simple mathematics of compounding, wherein a shorter duration leads to a higher exponential, or rather a “discount / multiplication factor”. Stocks which I have found suitable for such strategies are many, and some of the oft repeated ones are those at and above the “pop-midcap range”, wherein the equity enjoys a relatively liquid options market. Absent a liquid market, the bid-ask spread can often turn prohibitive into applying such strategies.

Now, I have previously discussed specific instances when one may establish a position by selling put options – eg. when one is comfortable opening a position on a stock below a strike price / cost basis AND the selling of insurance via put options also yields sizeable returns on an annual basis. Since, the cost basis serves as a downside protection for a full position in the underlying, an investor is expected to undertake fundamental analysis prior opening a position on the contracts.

Using Equity as a Hedge to “Selling Insurance”

Keeping this theme in mind and without bogging ourselves down with the first and second order option derivatives, let us assume a simple instance wherein an investor has sold 10 put contracts on stock XYZ at a strike price of $10 when the stock was trading at $17.50 with a duration of 2 months. Two weeks from expiry, markets and the stock (one may assume a high beta), take a turn for the worse and the stock price has moved towards $12 per share. At this stage, if the investor now changes his mind about opening the said position in case the options are assigned, he may engage in hedging the exposure to the underlying by shorting the equity.

Since theory states, that continuous delta hedging arbitrages away any excesses inherent in the option, one could decide to hedge away the delta of the underlying. At a price of $12 per share, the delta would be somewhere close to the 40 range. If the investor decides that, he wants to cancel out the exposure to the contract, he may also apply the premiums which will be potentially earned if the options expire worthless so as to decide a price at which he can close out his short position, after establishing a level at which he may decide to open a short sale on the stock. Alternatively, If the investor or the trader has a directional view, he may also decide to hedge basis his decided position size and future outlook for the equity of the underlying.

A right amount of thorough research and thought will surprise those who investigate the above strategy which incidentally is based on a bedrock of fundamental analysis. Therein lies the beauty and the catch-22: that every form of investing is fundamental and value investing, everything else is speculation and trading.

“Closing Time”

To close, I will have to and will be replacing the current IHRT bonds with another non-participating security trading at an attractive price given that they expire in May this year. Additionally, there exist a few opportunities which also display qualities similar to those of Figs late in 2024 or early 2025, when it was subject to a takeover bid by Story3 Capital.

As for the existing dry powder, I intend to deploy the monies so as to redistribute and equalize the portfolio holdings or into an exceedingly attractive opportunity. With the FIFA World Cup just around the corner, this is going to be an interesting time for the people of North America, as well as the stock markets. So far so good…